Risk Premium Calculation

Most of us already know how car insurance works. Every month or every year you pay a set amount to an insurance company. If you ever have an accident, you do not have to worry about the cost. Without insurance, one bad day could wipe out a large pile of money. With insurance, you give up a small, predictable amount on purpose. In return, you are protected from a much bigger loss.

That small payment has a name in economics and finance. It is your risk premium. The insurance company looks at your driving history, estimates how likely you are to have an accident, and sets a premium that matches that risk. You happily pay it, because handing over a little money for certain feels better than gambling on a large loss.

On this page we explain what the risk premium really means. Then we show how to work it out, both by hand and inside Decision Tree Analyzer.

A risk premium is the amount of money you are willing to give up just to avoid taking a risk. You hand that money to someone else, and in return they carry the risk for you. The insurance company is exactly that someone.

An example

Let's use the same example we walked through in the documentation for "Certainty Equivalent Calculation".

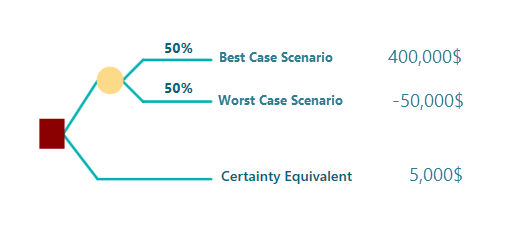

Imagine you have put together a business plan. To run it, you need to invest $50,000. If it works, you expect to make $400,000 in profit within a year. But it is a coin flip. There is a 50% chance it pays off, and a 50% chance you lose the whole $50,000 and earn nothing.

A friend likes your plan so much that he offers to buy it from you for $5,000. The deal is simple. You walk away and never run the plan, and he takes it over. He puts up the money, he carries all the risk, and you pocket a guaranteed $5,000 for giving up the opportunity.

If you work out the Expected Monetary Value (EMV) of the business opportunity, you get this:

EMV = 0.5 × $400,000 + 0.5 × (-$50,000) = $175,000

So here is the real question. Would you give up a deal worth $175,000 on paper for a sure $5,000? If your answer is yes, then your Certainty Equivalent is $5,000. That is the guaranteed amount you would happily accept instead of taking the gamble.

The Risk Premium is simply the gap between the Expected Monetary Value and the Certainty Equivalent.

So the Risk Premium works out to:

RP = EMV - CE

= $175,000 - $5,000

= $170,000

Why would anyone give up a deal for such a low Certainty Equivalent? You would do it when the risk really scares you and you want it gone at any cost. Maybe you simply cannot afford to lose $50,000 if things go wrong. When you take the sure $5,000 instead of the gamble, you are paying $170,000 as your Risk Premium. That is the price of peace of mind. It is a big number here because the deal is risky and the sure thing is small. That tells you this person is very risk averse.

Risk Premium in Decision Tree Analyzer

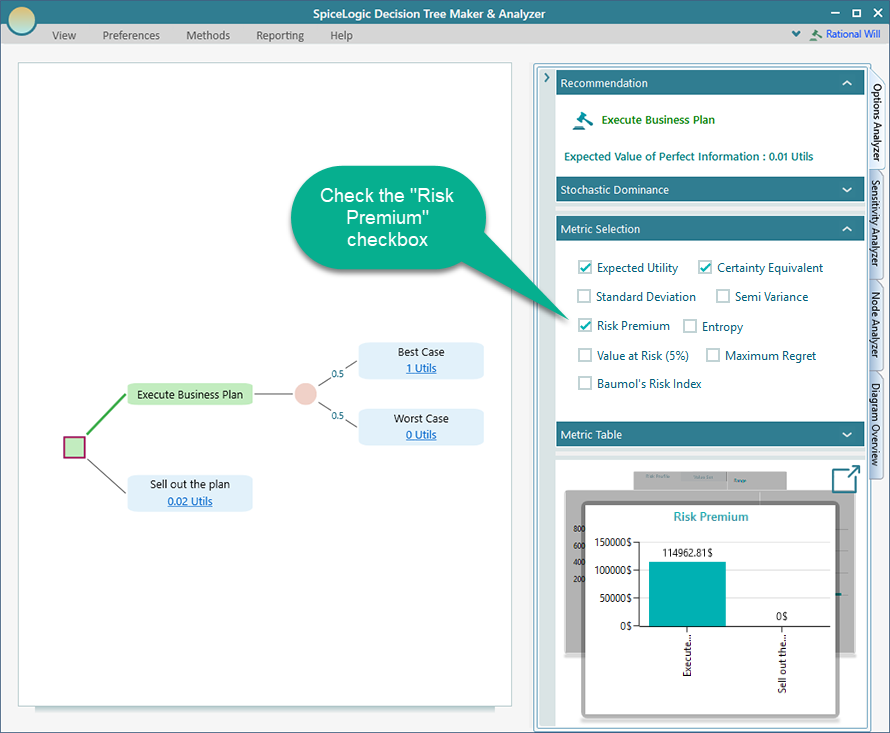

We showed how to build a Utility function and add it to a Decision Tree in the "Certainty Equivalent Calculation" example. Getting the Risk Premium follows the same steps you used there to get the Certainty Equivalent. In the same Metric panel where you picked the metrics, you will find a checkbox labeled "Risk Premium". Tick that checkbox, and the Risk Premium chart shows up next to the others in the Charts Carousel.

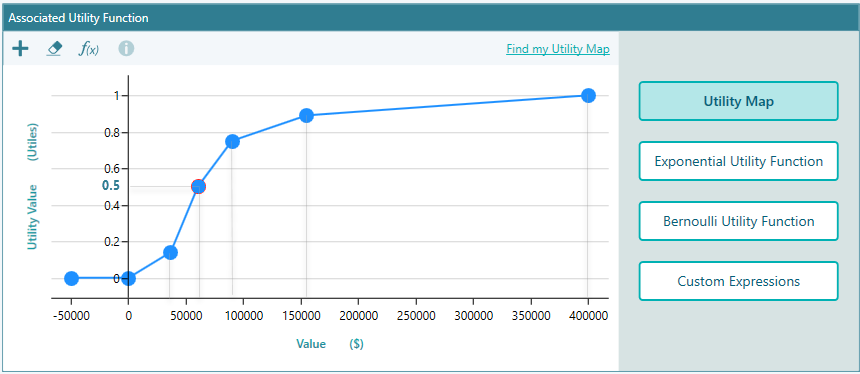

Remember the Utility Function we built earlier in the Certainty Equivalent Calculation example? We will use that same model here. A utility function captures how you personally feel about money. A guaranteed dollar is worth more to a cautious person than the same dollar dangling at the end of a risky bet. That is what turns a plain EMV into a Certainty Equivalent you would actually accept. For example, a careful business owner with bills to pay will treat a sure $60,000 as far more valuable than a coin-flip shot at much more, and the utility function puts that feeling into numbers.

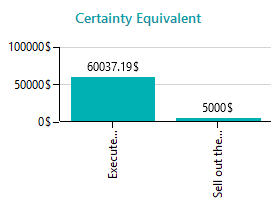

Using that utility function, the software gave us a Certainty Equivalent of $60,037.19. In plain terms, this is the guaranteed cash amount that feels just as good to this decision maker as taking the risky business gamble. Notice it sits well below the $175,000 EMV. That is exactly what you expect from someone who does not love risk. The bigger the gap, the more this person dislikes uncertainty.

We already calculated the Expected Monetary Value: EMV = $175,000. Putting both numbers into the Risk Premium formula gives:

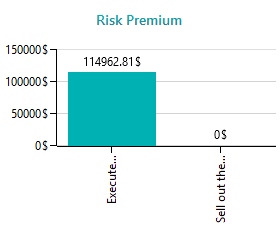

RP = EMV - CE = $175,000 - $60,037.19 = $114,962.81

So this decision maker would give up about $114,962.81 of expected value to swap the risky gamble for a sure thing. That is what they will pay, in expected dollars, to sleep well at night. Decision Tree Analyzer works this out for you automatically and shows the Risk Premium in the Chart Carousel, just as you see here.